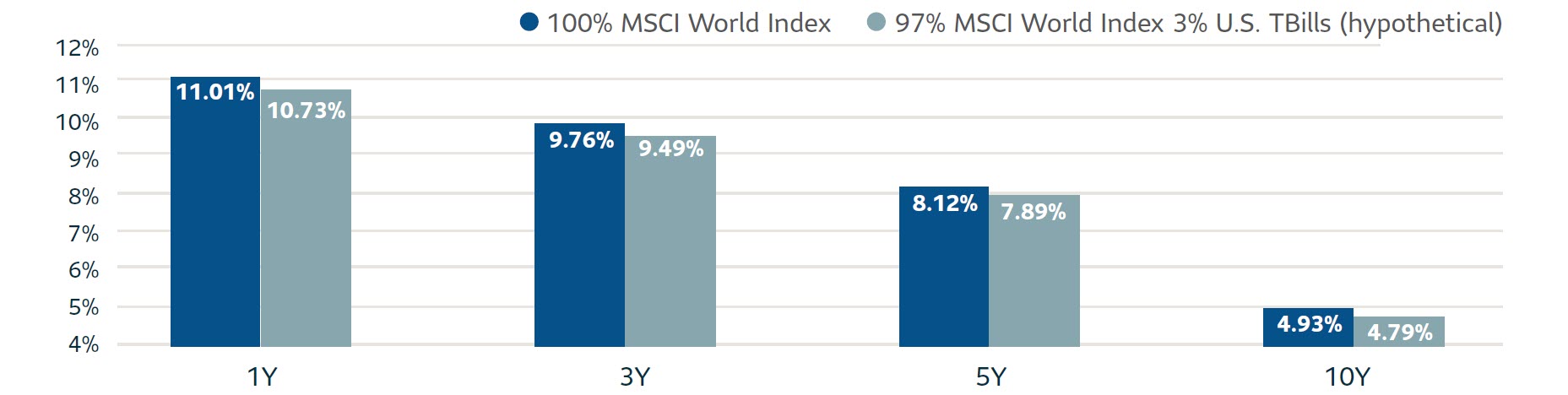

Institutional investors may carry cash in their portfolios for a variety of reasons, but often it is for liquidity. A cash equitization overlay program can provide liquidity without cash drag on a portfolio’s performance. This program replicates the macro market exposure of the policy portfolio, aiming to improve portfolio return and reduce tracking error over the long term.