Source: Chetty, Raj, John N Freidman, Nathaniel Henderson and Michael Spencer, 2020 How Did COVID-19 and Stabilization Policies Affect Spending and Employment? A New Real-Time Economic Tracker Based on Private Sector Data.

Changes in Consumer Spending RAJ CHETTY

Health concerns drive spending reductions among top earners

Government data has already confirmed that the pervasive drop in GDP was driven by an implosion in consumer spending.

Chetty’s research provides context and actionable insight to complement these overarching trends. With the use of ZIP code data, he determined that the massive drop in credit expenditure was concentrated in the most affluent ZIP codes. Almost two-thirds of the drop in credit card spending came from consumers in the top 25% of the income distribution. Those at the bottom 25% continue to spend at their pre-pandemic pace.

Survey results indicate that the drastic spending reduction by the rich was not driven by austerity, but rather health concerns. Nearly three-quarters of the drop in spending resulted from a reduction in services that required physical contact. For example, hotels and restaurants suffered because of their reliance on human interaction, but landscaping and poll installations were able to maintain revenue.

Small businesses data further supports Chetty’s conclusions. In affluent ZIP codes, small businesses lost 70% of their revenues from the pandemic’s onset, versus 30% in the lower rent areas. The revenue drop drove a comparable cut in the respective work forces.

The one-time household payments that arrived on April 15 were somewhat successful in that they drove a surge in spending. However, most spending was on durable goods, as consumers avoided in-person contact. This did little for many battered service sectors, and as a result, employment growth has lagged.

In-person service spending remains at half its normal level, and variations in states’ reopening plans had little impact on the difference in economic activity. Implicitly, consumers realize this is a health crisis and have in turn moderated in-person activity.

Paycheck protection did not reverse layoffs

The Federal Government’s solution to mitigating these job losses was its Paycheck Protection Program which gave loans to small businesses that would otherwise need to lay-off employees.

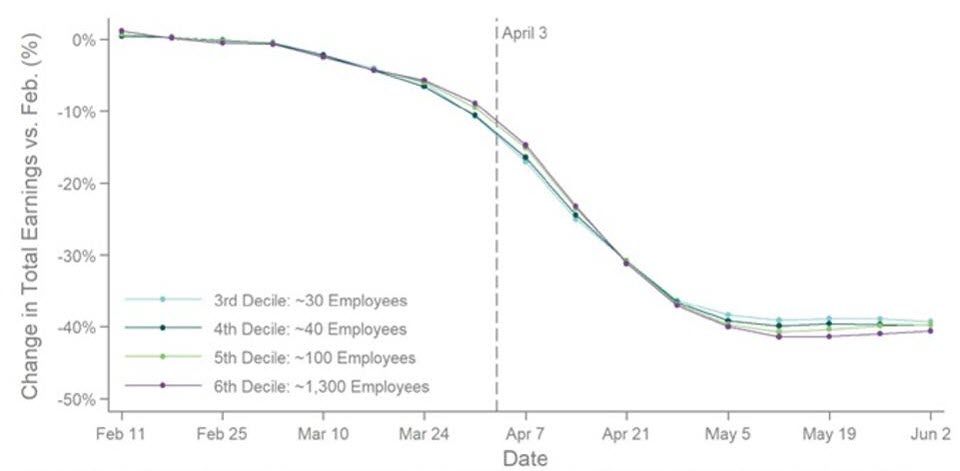

Yet despite the roll out of the Paycheck Protection Program, Chetty found that there was no difference in total earnings between a control group of smaller companies receiving PPP and a group of companies that did not qualify for those loans.

The dataset shows companies with average employee sizes of 10, 40 or 100 employees saw total earnings down about 40% from early February. This was right in line with large companies that on average have 1,300 employees.

Furthermore, states that had higher pre-PPP job losses did not see greater PPP participation. It appears companies that cut employees prior to PPP enactment didn’t reverse course; while companies that enacted minimal layoffs accepted support.

Impact of Paycheck Protection Program Loans on Employment