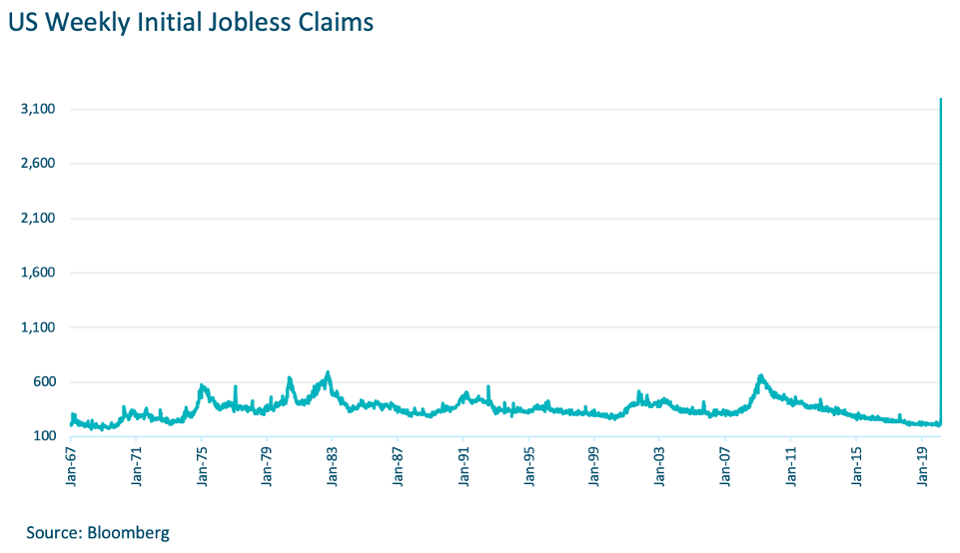

Over the coming weeks, layoffs will accelerate and the unemployment rate could eventually spike somewhere between 12 and 15% | SLC Management

The hope is that the summer months bring calm, with consumers starting to reengage and help stage a recovery. That certainly seems credible if social distancing flattens the infection curve and better testing helps with targeted containment. Nevertheless, a vaccine against COVID-19 is still 12-18 months away, even as countries and laboratories move rapidly to approve clinical trials.

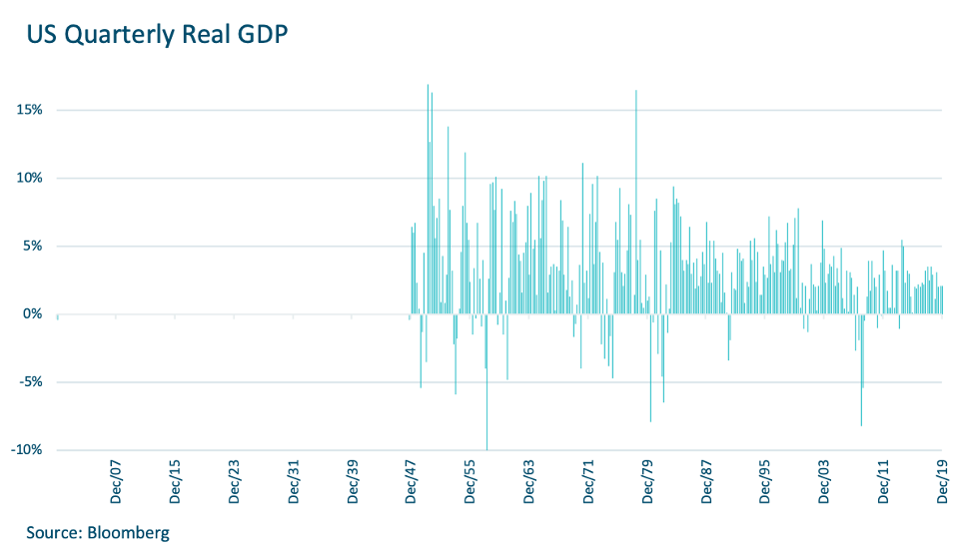

In this scenario, where growth pummeled in the first half, if over the second half growth recovers at around 5%, it would still leave the full year down over 6%. For perspective, the worst GDP showing since the end of World War II was 2009 with growth down 2.5%.

However, if the third quarter is disappointing and the U.S. doesn’t turn until close to the end of the year, annual GDP could be down over 8% with unemployment off the charts.

Market Leaders Will Fare Better

If the economy is down somewhere between 6% and 8%, annual corporate earnings could be cut by one-third to a half.

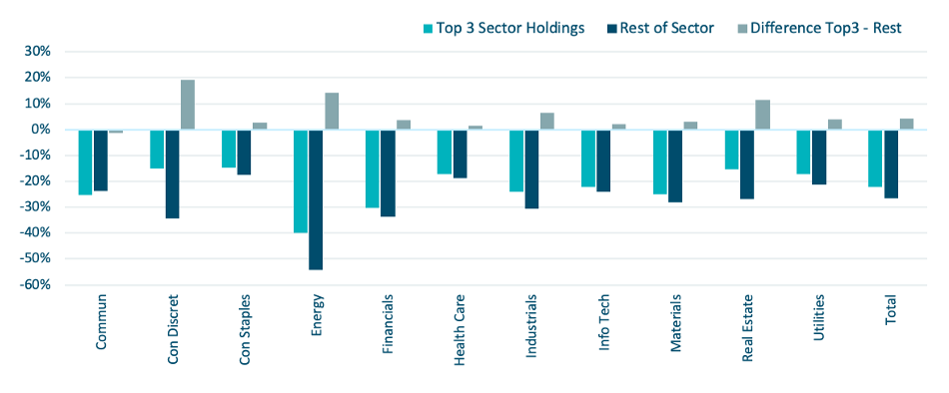

As in most downturns, larger well-fortified companies have an advantage as markets tend to conclude they have more staying power. As an example, since the equity market peak on February 19th, the S&P 500 is down 24.9% through the end of March. But the top 50 companies by market value are down only 19.7% while the bottom 50 are down 51.8%.

In a more robust measure of market leadership edge, a portfolio of the top three companies by market weight from each sector has outperformed the rest of the S&P 500 by 5.9% over the period from February 19th through March 31st.

S&P 500 Performance: Top 3 holdings versus rest of sector

From February 19, 2020 – March 26, 2020