Q2 2025: Investment Grade Private Credit update

Issuance activity overcame a slower start to the quarter to end at volumes exceeding Q1. Also, the continued uncertainties over global trade, inflation and fiscal policies highlight the potential benefits of IG private credit against this backdrop.

Market statistics for the private placement market sourced from Private Placement Monitor, a standard proxy for the investment grade (IG) private credit market. Other market data supplied by Bloomberg.

Markets

IG private credit activity started slowly in the second quarter of 2025. Both investors and issuers acted cautiously following market selloffs and wider credit spreads after international trade policies were announced by the U.S. administration. Despite the slower start into the second quarter, total issuance volumes exceeded the preceding quarter, with over US$36 billion across all private placement markets. Sector activity also shifted slightly during the second quarter, with more activity in the financial and utility sectors compared to the industrial sector.

Total issuance volume within corporate IG private debt remained on pace with the record-setting first half of 2024, with over US$69 billion issued year-to-date (compared to US$70 billion across the same period in the prior year). Investor demand continues to outstrip supply, driven by traditional insurance companies and a growing number of asset managers. Several broadly syndicated deals were more than 10-times oversubscribed, resulting in marginal price tightening relative to initial guidance. Despite intense competition for allocations, investors remained disciplined with no significant concessions on terms or covenants. Delayed funding structures remain common, reflecting strong issuers’ desire to secure robust terms and pricing ahead of potential volatility. Looking ahead, we expect continued competition over the second half of 2025.

Outlook

We continue to observe strong activity in the private credit market, driven by persistent institutional demand. As competition compresses spreads in public markets, we’ve seen investors increasingly turning to private credit for its yield premium. However, growing competition in the private space has, in some cases, reduced the spread differential between public and private markets. Managers seeking transactions representing potential value opportunities might need to consider bilateral and smaller club deals over broadly syndicated opportunities.

In focus

The role of IG private credit amid today’s volatility, uncertainty

The global economy is navigating a complex landscape, shaped by geopolitical uncertainty, market volatility and shifting monetary policies. Trade tensions between major economies have resurfaced, with new U.S. tariffs on Chinese and European goods and potential retaliatory measures threatening to disrupt supply chains. Inflation remains a concern in many developed markets, prompting central banks to maintain higher-for-longer interest rate policies. These dynamics have led to heightened market volatility and a more cautious lending environment.

Against this backdrop, IG private credit is gaining renewed attention, but also remains underrepresented in many portfolios. Once a niche corner of the fixed income universe, IG private credit has evolved into a robust, diversified and scalable market. With an estimated addressable market of US$40 trillion, it now spans corporate private placements, asset-backed finance (ABF) and bespoke capital solutions. In today’s environment, marked by rising tariffs, inflationary pressures and tighter credit conditions, IG private credit offers a potentially attractive combination of yield, quality and downside protection, characteristics that merit review in today’s changing landscape.

IG private credit’s risk-adjusted return profile

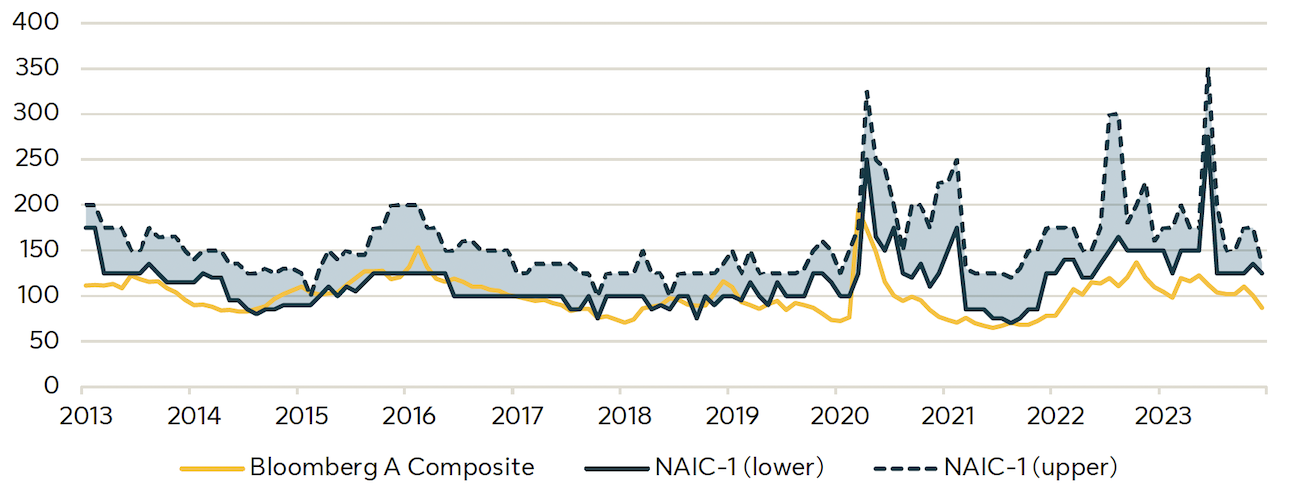

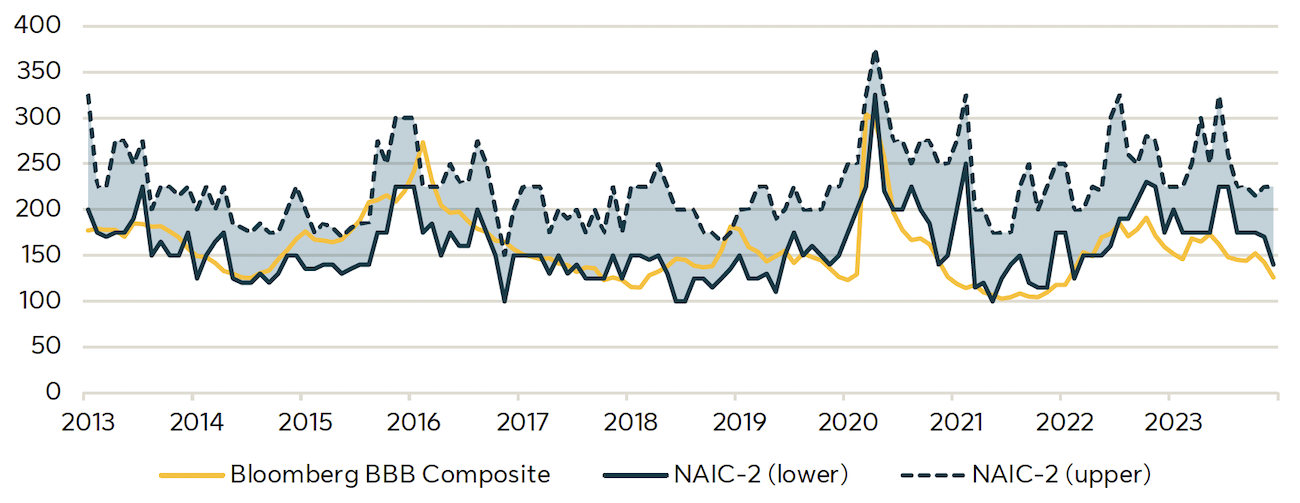

In yield-challenged environments, IG private credit offers a meaningful spread premium over comparable public investment grade bonds – often in the range of 75–200 basis points. This excess return is not simply a liquidity premium: it reflects the bespoke, complex nature of the deals that require extended negotiations directly with the issuers. As the following table illustrates, this yield premium has endured throughout various economic cycles.

Private placement NAIC-1 spreads vs. A-rated public corporate spreads (basis points)

Private placement NAIC-2 spreads vs. BBB-rated public corporate spreads (basis points)

Sources: Private Placement Monitor, Bloomberg, 2024. Private placement market spreads were sourced from the Private Placement Monitor using transactions with a 10-year average life. Bloomberg U.S. corporate spreads calculated based on average option-adjusted spreads to Treasury for Bloomberg A Corporate Total Return Index Value Unhedged USD (LCA1TRUU) and Bloomberg Baa Corporate Total Return Index Value Unhedged USD (LCB1TRUU) indexes with an average life of 10.6 years and 10.5 years, respectively. Past performance is not necessarily indicative of future returns. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur. It is not possible to directly invest in an index.

Potential benefits of structural protections and seniority

IG private credit transactions are typically structured with investor protections that public bonds might not provide. These might include:

- Secured or structurally senior positions.

- Enhanced covenant frameworks providing additional downside protection such as limitation on additional debt.

- Enhanced monitoring/reporting requirements.

- Financial covenants that not only provide for financial discipline but also operate as an early detection trigger if the credit metrics of the issuer deteriorates.

A strong covenant framework, in addition to a senior and/or secured position, provide essential downside protection and an early intervention tool in IG private credit transactions. In fact, well-structured private credit portfolios can actually outperform public portfolios of a comparable quality mix due to these strong mitigating factors.

Diversification and portfolio enhancement

IG private credit offers exposure to a broader range of sectors and structures, including corporate private placements, asset-backed loans and structured credit solutions. This can help investors diversify beyond common index sectors such as banking, consumer non-cyclicals and technology. Integrating IG private credit into a fixed income portfolio can enhance both yield and diversification. In fact, a select allocation to IG private credit can increase portfolio yield meaningfully without compromising credit quality.

Alignment with long-term liabilities

For institutional investors with long-dated liabilities, such as pension plans and insurance companies, IG private credit can offer duration-aligned, stable cash flows. These investments are typically held to maturity and can be tailored to match specific liability profiles. This speaks to another growing trend of increasingly deep ties between alternative asset managers and insurance companies given their strong symbiotic relationship. IG private credit can also play a pivotal role in enhancing the return profile of retirement portfolios without taking on undue risk.

Risk factors and addressing common concerns

IG private credit’s non-public and bespoke nature can provide investors with potential yield benefits and structural protections. While IG private credit is inherently illiquid, this illiquidity underlies the attractive characteristics of these assets.

The lack of an active market may also impact accurate and timely valuations. These concerns are increasingly addressed by a market that continues to mature:

- Liquidity is not binary, but a spectrum – investors can adjust a portfolio to meet their expected liquidity needs. Broadly syndicated transactions that are performing have demonstrated reasonable liquidity, whereas bilateral transactions likely have less liquidity.

- External data points are increasing – a growing number of IG private credit deals are being rated by major credit agencies.

- Open-ended investment structures, such as through a fund structure or separately managed accounts, enables institutional investors to tailor IG private credit exposure to specific liability profiles and regulatory constraints, fostering close manager collaboration on duration, risk tolerance and liquidity planning.

A strategic allocation for the future

In our view, IG private credit represents not just a tactical opportunity, but a strategic allocation positioning that can increasingly align with the evolving needs of institutional investors. In a world where investors may be searching farther afield for stronger returns or resilience, IG private credit can offer a powerful alternative, combining the credit quality of public markets with the customization, yield and protection characteristics of private markets.

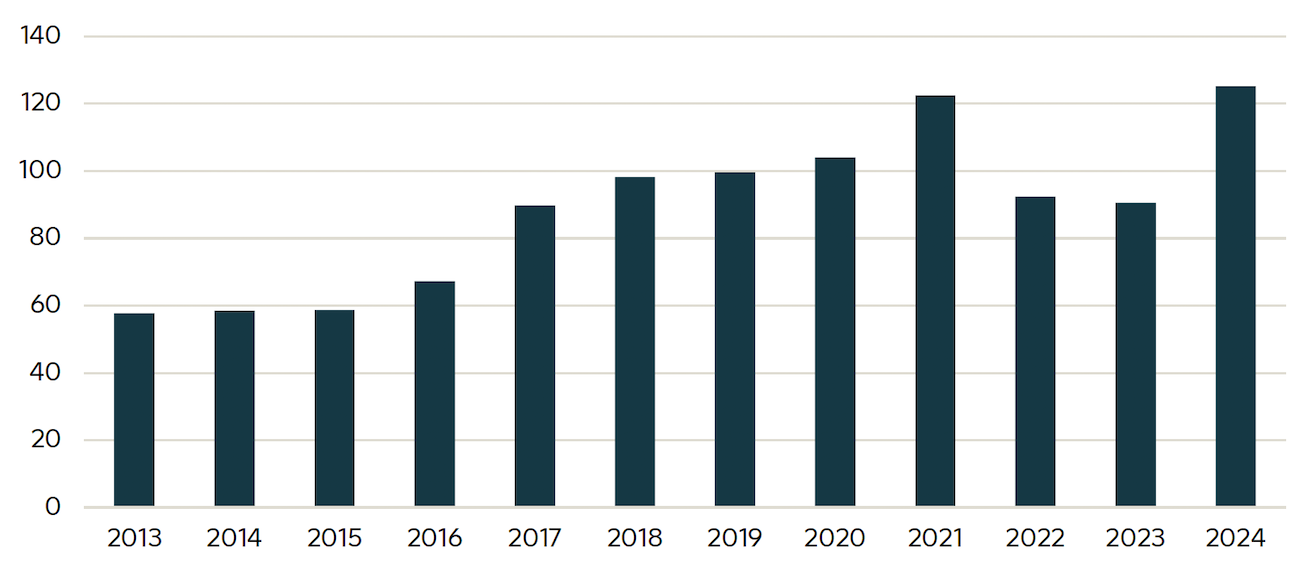

U.S. private placement market volume (US$, billions)

Source: Private Placement Monitor, as of June 2025. U.S. private placement market volume is defined as the total value of transactions of U.S. bonds not registered for open market public distribution and sold by issuing companies to pre-selected accredited investors, as tracked by Private Placement Monitor in a given year.

Disclosure

© 2025, SLC Management

Any reference to a specific asset does not constitute a recommendation to buy, sell or hold or directly invest in it. It should not be assumed that any investment will be profitable or will equal the results of the assets discussed in this document. Any assets referred to herein represent investments of SLC Fixed Income, which are managed on a discretionary and non-discretionary basis for Sun Life's General Account and certain third-party clients.

SLC Management is the brand name for the institutional asset management business of Sun Life Financial Inc. (“Sun Life”) under which Sun Life Capital Management (U.S.) LLC in the United States, and Sun Life Capital Management (Canada) Inc. in Canada operate. Sun Life Capital Management (Canada) Inc. is a Canadian registered portfolio manager, investment fund manager, exempt market dealer and in Ontario, a commodity trading manager. Sun Life Capital Management (U.S.) LLC is registered with the U.S. Securities and Exchange Commission as an investment adviser and is also a Commodity Trading Advisor and Commodity Pool Operator registered with the Commodity Futures Trading Commission under the Commodity Exchange Act and Members of the National Futures Association.

Unless otherwise stated, all figures and estimates provided have been sourced internally and are as of December 31, 2024. Unless otherwise noted, all references to “$” are in U.S. dollars. Past performance is not indicative of future results.

Nothing herein constitutes an offer to sell or the solicitation of an offer to buy securities. The information in these materials is provided solely as reference material with respect to the Firm, its people and advisory services business, as an asset management company.

Market data and information included herein is based on various published and unpublished sources considered to be reliable but has not been independently verified and there is no guarantee of its accuracy or completeness.

This content may present materials or statements which reflect expectations or forecasts of future events. Such forward-looking statements are speculative in nature and may be subject to risks, uncertainties and assumptions and actual results which could differ significantly from the statements. As such, do not place undue reliance upon such forward-looking statements. All opinions and commentary are subject to change without notice and are provided in good faith without legal responsibility. Unless otherwise stated, all figures and estimates provided have been sourced internally and are current as at the date of the paper unless separately stated. All data is subject to change.

This information is not intended to provide specific financial, tax, investment, insurance, legal or accounting advice and should not be relied upon and does not constitute a specific offer to buy and/or sell securities, insurance or investment services. Investors should consult with their professional advisors before acting upon any information contained in this paper. An investor may not invest directly in an index.

No part of this material may, without SLC Management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

This material is intended for institutional investors only. It is not for retail use or distribution to individual investors. Nothing in this presentation should (i) be construed to cause any of the operations under SLC Management to be an investment advice fiduciary under the U.S. Employee Retirement Income Security Act of 1974, as amended, the U.S. Internal Revenue Code of 1986, as amended, or similar law, (ii) be considered individualized investment advice to plan assets based on the particular needs of a plan or (iii) serve as a primary basis for investment decisions with respect to plan assets.

Data presented in this article have been calculated internally based on external market data sourced from Private Placement Monitor and other sources. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments.

Investment-grade credit ratings of our private placements portfolio assets are based on a proprietary, internal credit rating methodology that was developed using both externally purchased and internally developed models. This methodology is reviewed regularly. More details can be shared upon request. There is no guarantee that the same rating(s) would be assigned to portfolio asset(s) if they were independently rated by a major credit ratings organization.

Investments involve risk, including loss of principal. Diversification does not guarantee against loss or ensure a profit. Nothing herein constitutes an offer to sell or the solicitation of an offer to buy securities. The information in these materials is provided solely as reference material with respect to the Firm, its people and advisory services business, as an asset management company.

SLC-20250730-4697970