Market Review

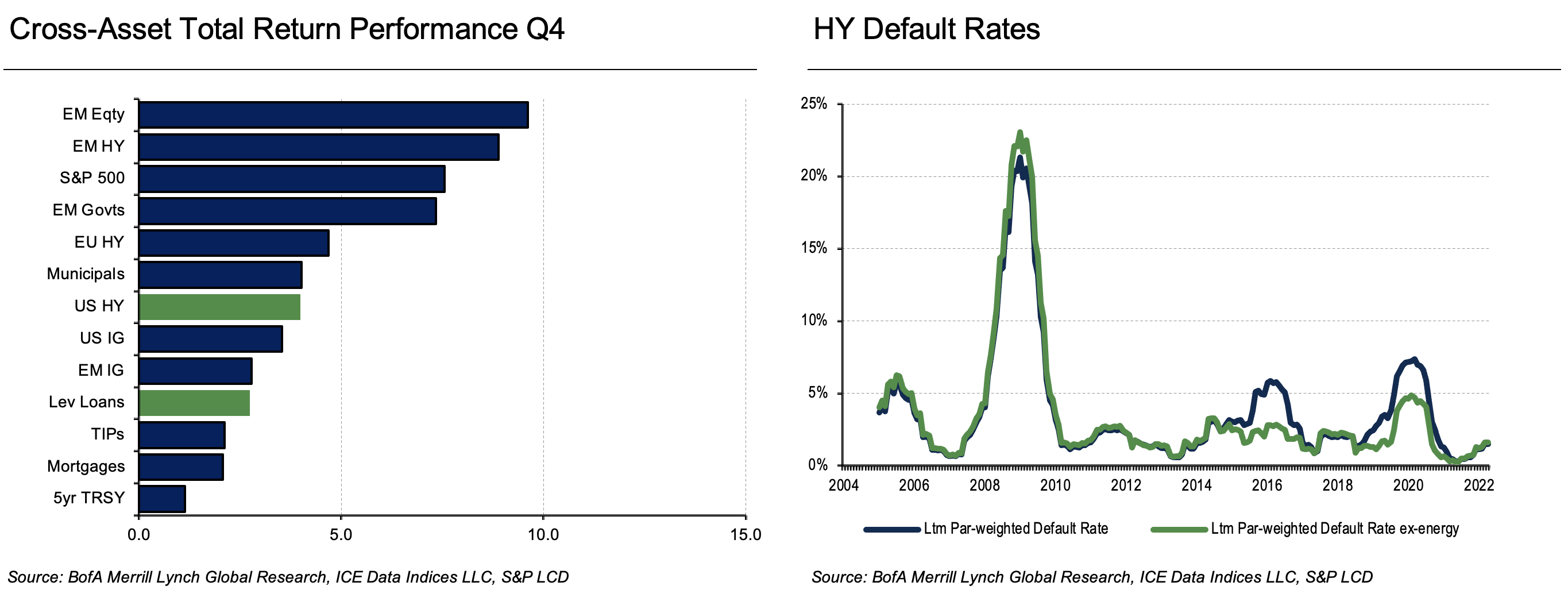

In the final quarter of 2022, all fixed income markets rallied retracing some of the losses sustained during the year, though most of them still finished the year in the red. More specifically in Q4, US high yield bonds generated +3.98% as measured by the ICE BAML US High Yield index and leverage loans returned +2.74% as measured by the Morningstar LSTA Leveraged Loan index. For the year, leveraged loans significantly outperformed all other major asset classes with a return of -0.60%, while US High Yield, European High Yield, US Investment Grade, TIPs, Mortgages, Emerging Market High Yield and Investment Grade and the S&P 500 Index all closed the year with double-digit negative returns.

During the quarter, the US Fed still continued to combat inflation and raised rates twice, 75 basis points in November and 50 basis points in December. Some investors believe the Fed may pause rate hikes after CPI prints came in below expectations consecutively in November and December and chair Powell was less hawkish than feared at the January FOMC meeting after delivering a 25 basis point rate hike.

US Treasury yield moves were mixed; the 10-year ended the quarter at 3.87% (up 5 basis points since Q3 and up 274 basis points since the start of the year) and the 5-year ended at 4.00% (down 9 basis points since Q3 but up 236 basis points since the start of the year). Yields and spreads tightened in high yield bonds, ending Q4 at 8.99% and 491 basis points respectively, and in leveraged loans, yields tightened to 9.99%. WTI oil prices ended Q4 at $80.26/ barrel, mostly unchanged from last quarter and up 7% since the start of the year. The S&P 500 returned +7.55% in Q4 and -18.13% for the year.