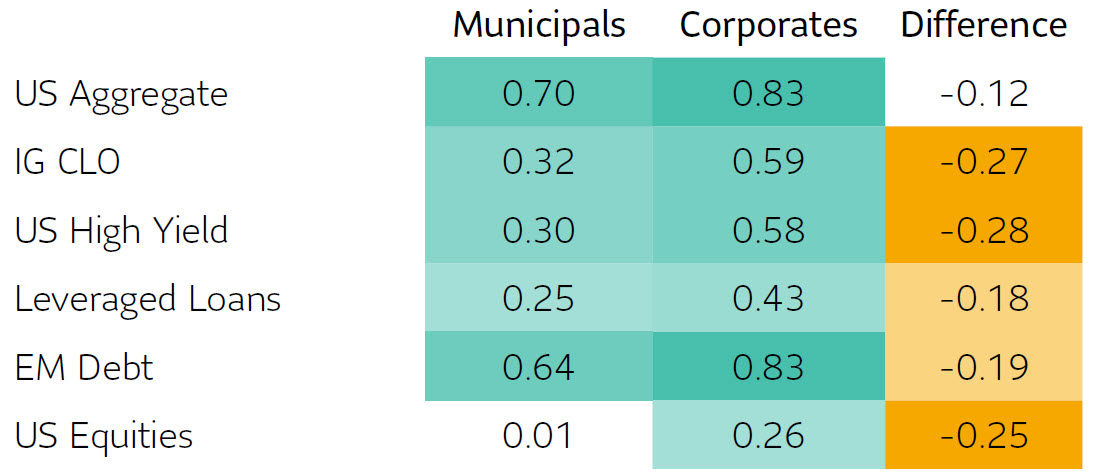

Municipal bond yields rose sharply due to the large-scale selloff in the first half of 2022, providing an attractive entry point for institutional buyers with cross-over bond portfolios. Historically, municipal bonds have shown higher levels of resilience compared to corporate bonds – showcasing lower default rates, less correlation to risk assets, and diversified cash flow streams backed by essential services. As recession is front of mind for investors across the globe, we believe now is the time for bond buyers to reconsider municipals.

Where was the municipal bond market before this recent selloff?

Compared to corporate bonds, municipal bonds offered little relative value to cross-over buyers. This is because the Tax Cuts and Jobs Act of 2017 lowered the U.S. corporate tax rate to 21% from 35%. Consistent demand from high tax-bracket retail buyers have kept prices high and spreads tight for several years.

Relative to corporate bonds, municipal bond valuations are often influenced by supply/demand technicals. Retail flows are fickle and supply varies month to month, creating swings in valuations not related to credit quality. The absence of large institutional buyers over the past five years has exacerbated this volatility.

Why are they back?

Since late 2021, the municipal bond market has seen significant outflows, providing an attractive entry point for institutional investors.

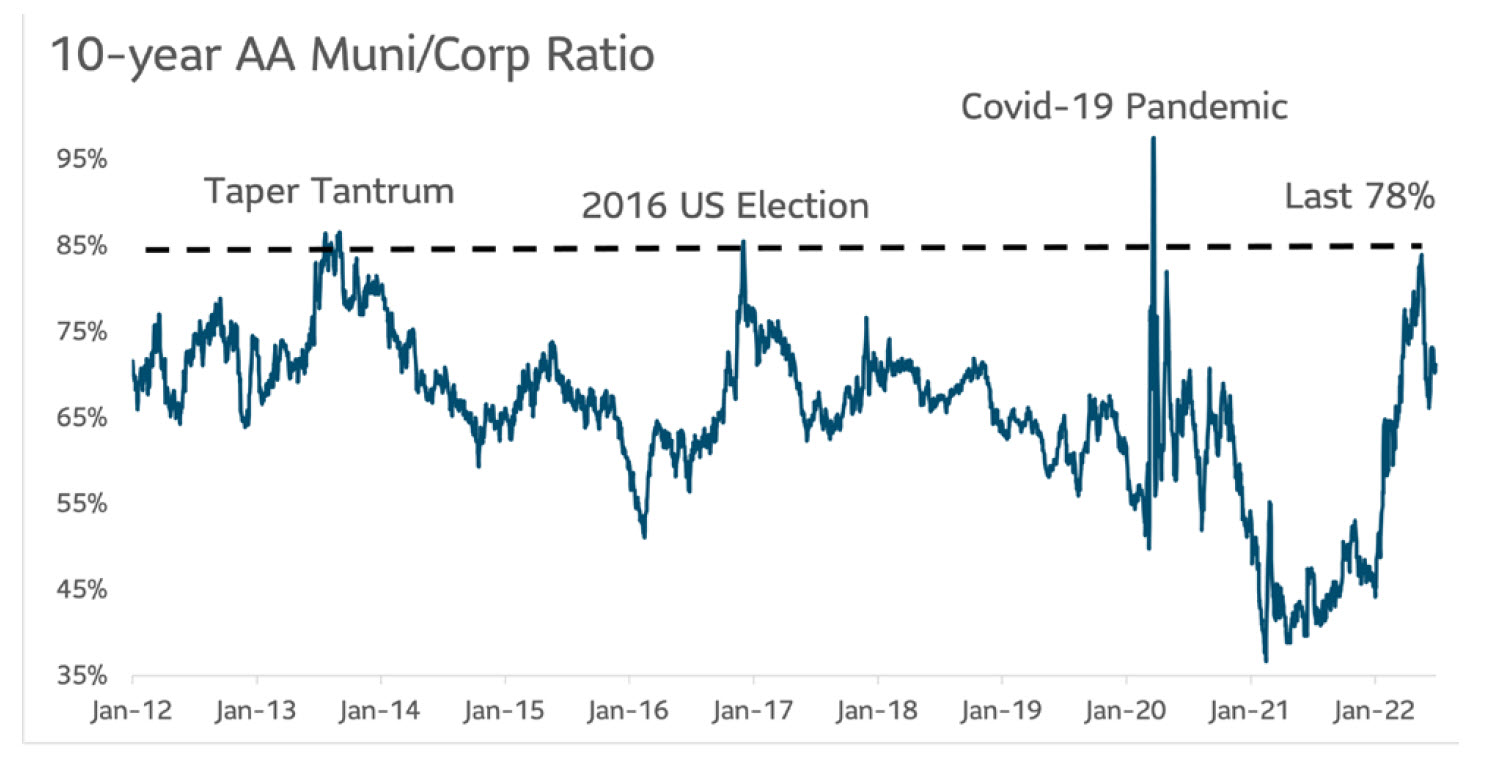

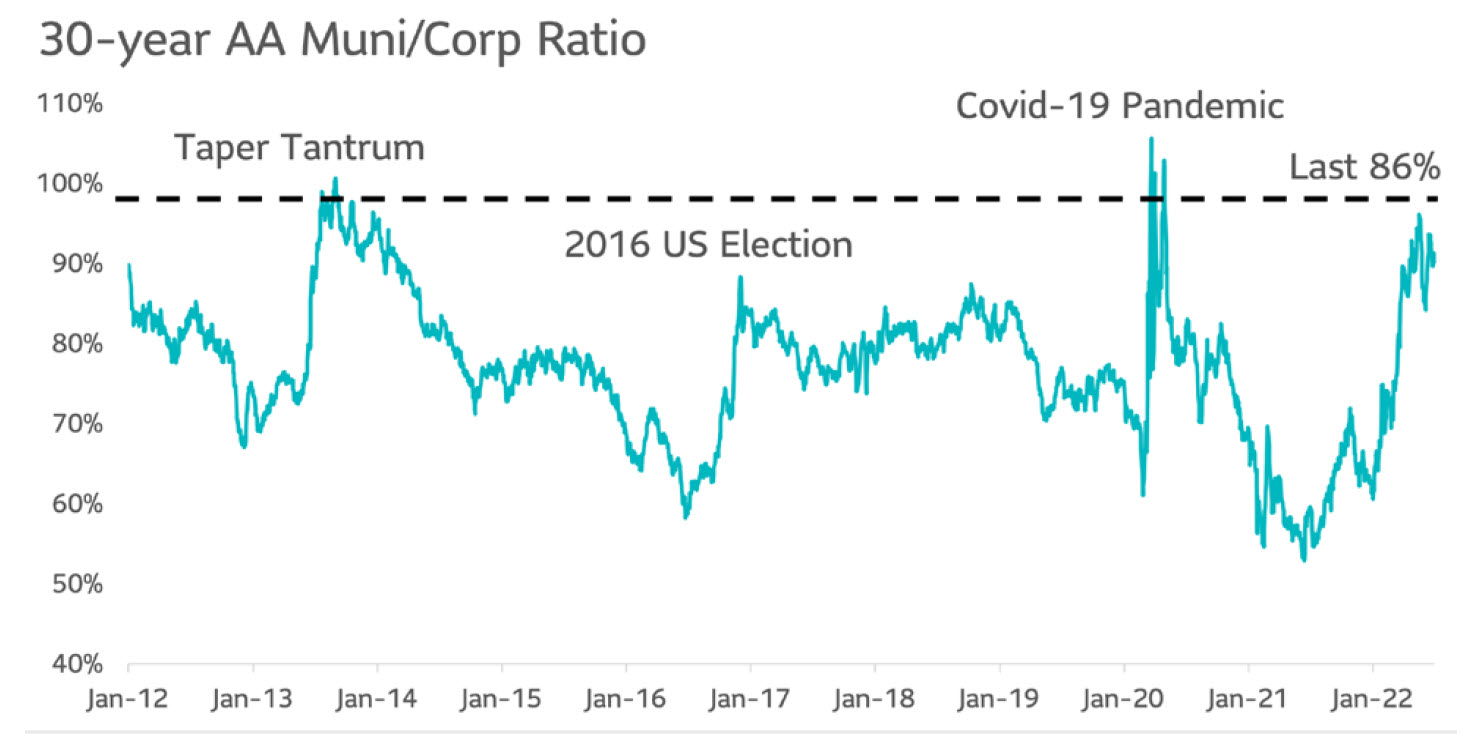

The Bloomberg IG Municipal Bond index returned -8.98% in the first half of 2022, as retail money left the space due to intense market volatility. As a result, muni yields climbed higher as prices have fallen, and muni/corporate ratios – which measure the relative value of tax-exempt municipal bonds to equal-tenor corporates – have returned to pre-tax reform levels (excluding the COVID-19-induced selloff). These higher yields make munis an attractive option for investors looking to add credit exposure to a cross-sector bond portfolio.

Net new issuance currently trails most annual estimates but could pick up speed later in the year if Treasury yields stabilize. This trend, coupled with reduced outflows, could present a tailwind for performance for the balance of 2022.