Currency forwards and cross-currency swaps can be used to manage the currency risk of foreign investments.

- Currency forwards are typically used for investments that have a high degree of uncertainty in the timing and amount of future cash flows such as public equity or high yield debt. Given the cash flow uncertainty, this approach is based on the market value of the investment instead of the individual cash flows. Forward contracts with short dated maturities have the liquidity and low transaction costs necessary for efficient dynamic rebalancing to match fluctuations in foreign asset values.

- Cross-currency swaps are commonly used for fixed income investments where the cash flows are known with a high degree of certainty. Hedging currency risk with a cross-currency swap effectively creates a synthetic local currency denominated bond by converting the bond’s foreign currency denominated cash flows or risk into a stream of local currency payments. Cross currency swap hedging strategies can be tailored for either active strategies or passive buy-and-hold fixed income strategies.

Cross currency swaps are Over the Counter (OTC) derivative instruments that involve exchanging interest and principal payments in two different currencies. Each side of the swap can be either fixed or floating payments. To facilitate the purchase of foreign assets, an initial currency exchange may be included. Similar to other OTC derivative instruments, a daily mark-to-market of collateral is required.

Offsetting currency risk for passive buy-and-hold portfolios (cash flow matching)

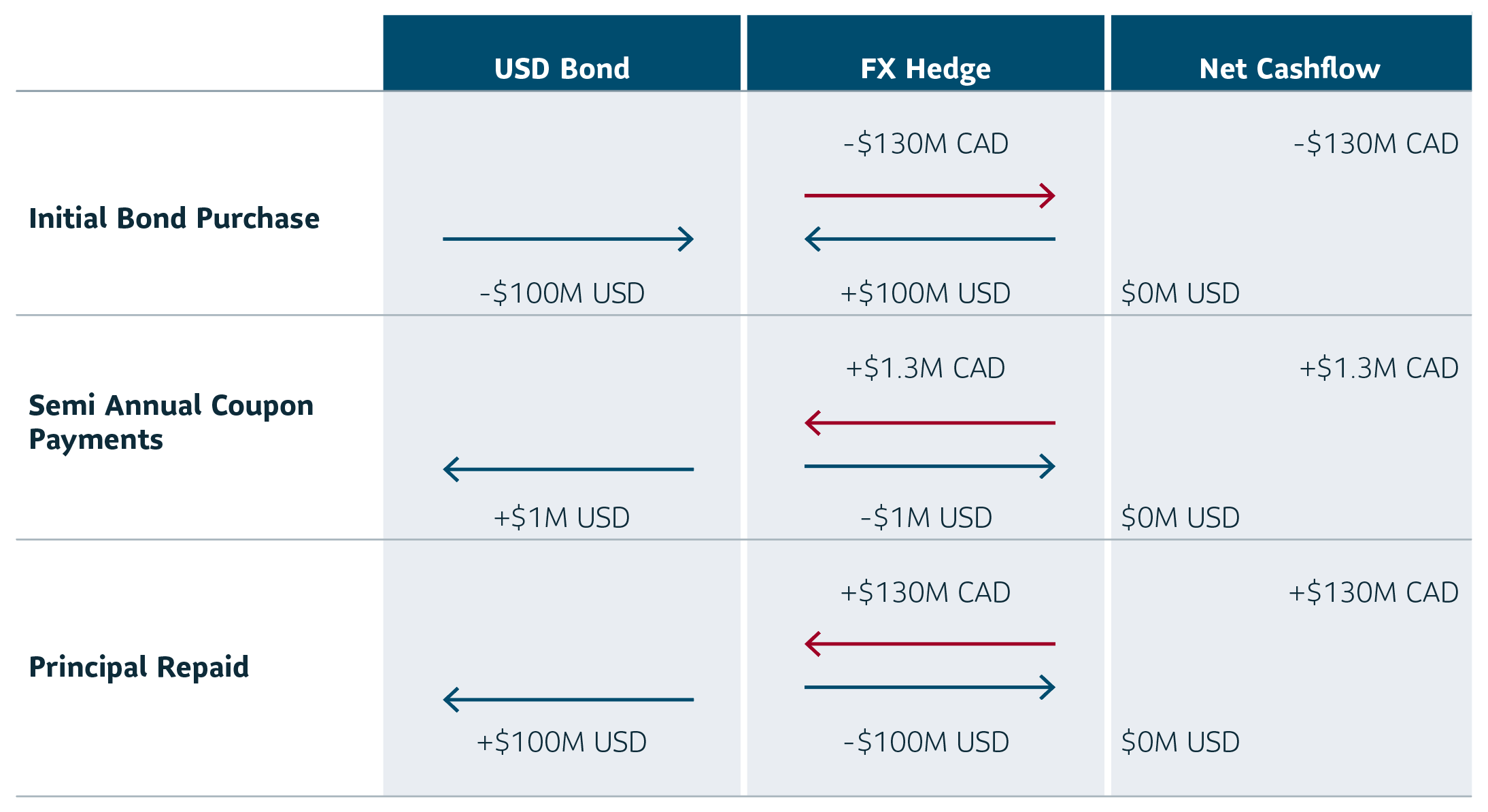

For investors with buy-and-hold mandates where bonds are held to maturity, currency risk can be offset at the cash flow level. When a foreign bond is purchased, a cross-currency swap is included to pay foreign coupons and receive payments in the domestic currency.

Since the cash flows of each individual bond are matched with a cross currency swap, this strategy requires little ongoing maintenance. Although the cash flows are matched, the interest rate sensitivities of the two assets are not equal. The market values of the cross currency swap and bond fluctuate over time as interest rates or credit spreads fluctuate.

Example: Canadian investor owns a USD $1 million face value

U.S. corporate bond with 2% coupon rate, paid semi-annually.

*Cash flows from investor’s perspective

For Illustrative purposes only.

Offsetting currency risk for active portfolios (risk matching)

Offsetting currency risk at the portfolio level may be more suitable for investors with active mandates that have more turnover in their portfolios. This is because entering and unwinding individual cross-currency swaps for each position would be operationally burdensome. By offsetting the interest rate risk at different key rate durations (KRD), the portfolio’s sensitivity to foreign interest rate risk will be offset and the exposure will be transferred to domestic interest rate exposure.

Risk matching will require rebalancing as the portfolio’s composition and duration profile changes. Since this is performed at the portfolio level, risk matching should decrease the turnover for currency swap positions for granular portfolios with many holdings. Unlike a cash flow matching approach, risk matching offsets the foreign interest rate sensitivity, not the individual foreign cash flows.

Example: Canadian investor owns a portfolio of U.S. bonds

For a Canadian investor holding a portfolio of U.S. bonds, U.S. interest rate risk can be offset using a portfolio of cross currency swaps by paying fixed USD payments and receiving fixed CAD payments. Paying fixed in USD will act to offset U.S. interest rate risk while receiving fixed in CAD will introduce exposure to Canadian interest rates.

U.S. Key Rate Duration Exposure*

| 2Y | 5Y | 10Y | 20Y | 30Y | Total | |

|---|---|---|---|---|---|---|

| Bond Portfolio | 5,000 | 15,000 | 20,000 | 15,000 | 5,000 | 60,000 |

| Cross Currency Swap: Pay Leg | (5,020) | (14,776) | (20,034) | (14,960) | (5,210) | (60,000) |

| Mismatch | (20) | 224 | (34) | 40 | (210) |

0 |

*Key Rate Duration Measured in USD DV01. For illustrative purposes only.

Canadian Key Rate Duration Exposure*

| 2Y | 5Y | 10Y | 20Y | 30Y | Total | |

|---|---|---|---|---|---|---|

| Cross Currency Swap: Receive Leg | 5,649 | 15,941 | 20,242 | 14,642 | 4,986 | 61,460 |

* Key Rate Duration Measured in CAD DV01. For illustrative purposes only.

Key rate duration measures a portfolio’s sensitivity to interest rates at different points on the yield curve. While offsetting portfolio duration will protect against parallel moves in yields, using key rate durations allows an investor to manage changes in the shape of the yield curve in addition to the level of yields.

Considerations

OTC instruments can be complex, which is why it is important to work with an experienced asset manager. OTC derivatives tend to have less liquidity than those that are exchange traded. SLC Management has extensive experience trading OTC derivatives, including cross currency swaps. OTC instruments also involve counterparty risk, for which we have established policies and procedures to manage credit risk of all counterparties.

At SLC Management, we focus on developing strong dealer relationships to secure competitive pricing across geographies. Cross currency swaps can be a useful tool to manage currency risk in foreign bond investments by transforming foreign coupon payments to domestic cash flows. This can be done by either offsetting the cash flows of each bond individually or by targeting interest rate risk at various key rate durations. Our clients benefit from cross currency swaps because they are highly customizable and well suited to managing the currency risk of foreign fixed income investments.

This paper is intended for institutional investors only. The information in this paper is not intended to provide specific financial, tax, investment, insurance, legal or accounting advice and should not be relied upon and does not constitute a specific offer to buy and/or sell securities, insurance or investment services. Investors should consult with their professional advisors before acting upon any information contained in this paper.

SLC Management is the brand name for the institutional asset management business of Sun Life Financial Inc. (“Sun Life”) under which Sun Life Capital Management (U.S.) LLC in the United States, and Sun Life Capital Management (Canada) Inc. in Canada operate. Sun Life Capital Management (Canada) Inc. is a Canadian registered portfolio manager, investment fund manager, exempt market dealer and in Ontario, a commodity trading manager. Sun Life Capital Management (U.S.) LLC is registered with the U.S. Securities and Exchange Commission as an investment adviser and is also a Commodity Trading Advisor and Commodity Pool Operator registered with the Commodity Futures Trading Commission under the Commodity Exchange Act and Members of the National Futures Association. Registration as an investment adviser does not imply any level of skill or training.

Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives involves leverage and could lose more than the amount invested. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio.

Unless otherwise stated, all figures and estimates provided have been sourced internally and are as of March 31, 2020. Unless otherwise noted, all references to “$” are in U.S. dollars.

Nothing in this paper should (i) be construed to cause any of the operations under SLC Management to be an investment advice fiduciary under the U.S. Employee Retirement Income Security Act of 1974, as amended, the U.S. Internal Revenue Code of 1986, as amended, or similar law, (ii) be considered individualized investment advice to plan assets based on the particular needs of a plan or (iii) serve as a primary basis for investment decisions with respect to plan assets.

This document may present materials or statements which reflect expectations or forecasts of future events. Such forward-looking statements are speculative in nature and may be subject to risks, uncertainties and assumptions and actual results which could differ significantly from the statements. As such, do not place undue reliance upon such forward-looking statements. All opinions and commentary are subject to change without notice and are provided in good faith without legal responsibility.

Unless otherwise stated, all figures and estimates provided have been sourced internally and are current as at the date of the paper unless separately stated. All data is subject to change.

No part of this material may, without SLC Management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

© 2020, SLC Management