Real "risk-free' rates since 1311, single-issuer basis BANK OF ENGLAND

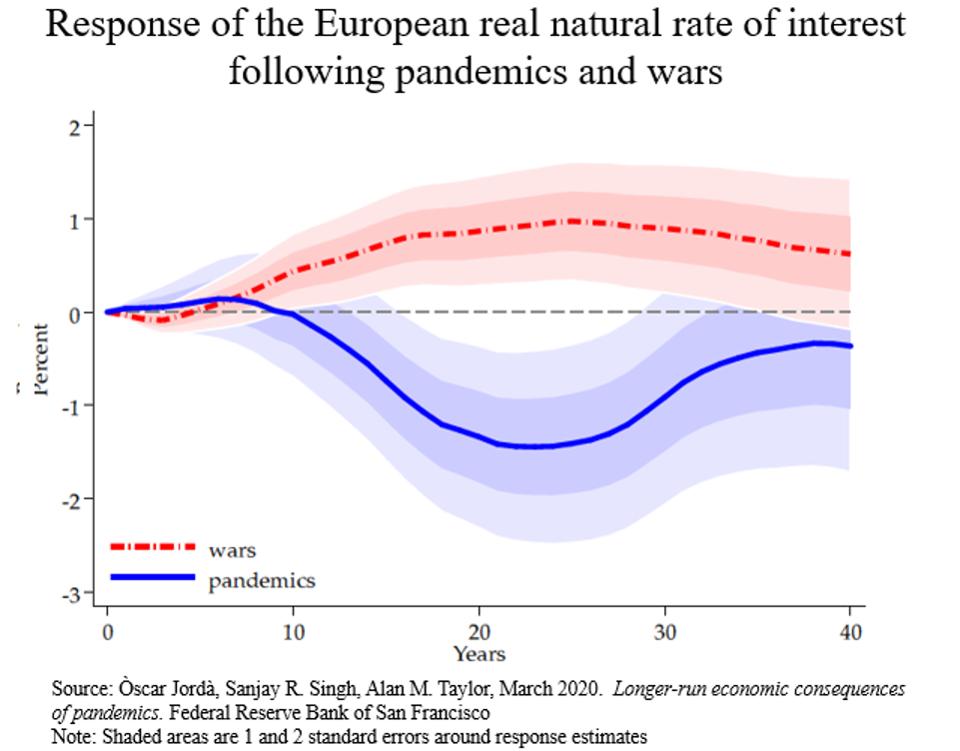

Meanwhile, other researchers have hypothesized that once countries become more stable and the incidence of wars mitigates, the reduction in geopolitical risk tends to dampen real rates.

The End To The Current Era of Globalization?

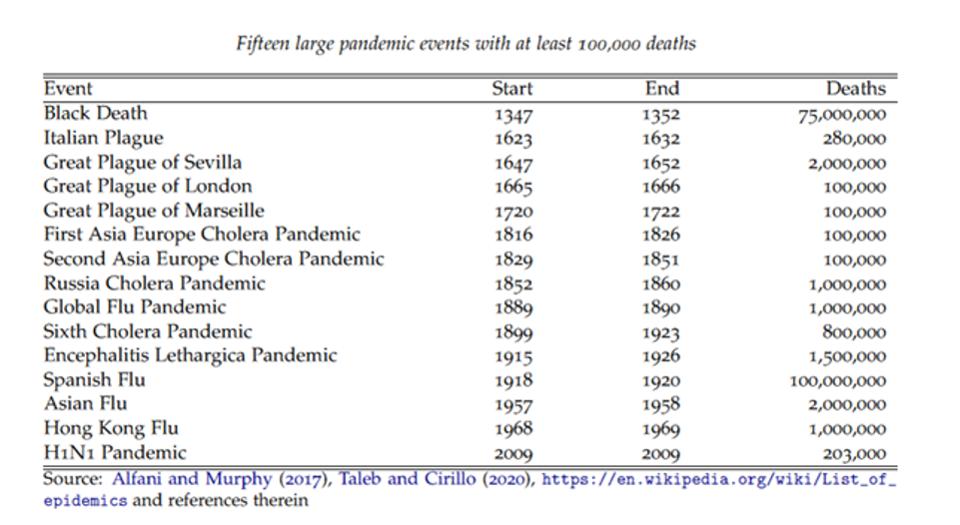

The aftermath of many of Europe’s pandemics was also a reduction in trade. While trade links ushered in a higher standard of living pre-crisis, any related health scare usually led to a pullback. When the Spanish Flu ended so did the first era of industrial globalization that was already under siege from the tensions of World War I.

And so today, COVID-19 may bookend the apex of global supply chains developed over the last two decades with China at its hub. Prior to the virus, the U.S. was threatening tariffs on major trading partners to help reset relationships. Now that the virus has exposed potential supply vulnerabilities, it may accelerate reshoring – particularly for any production or process remotely related to national security.

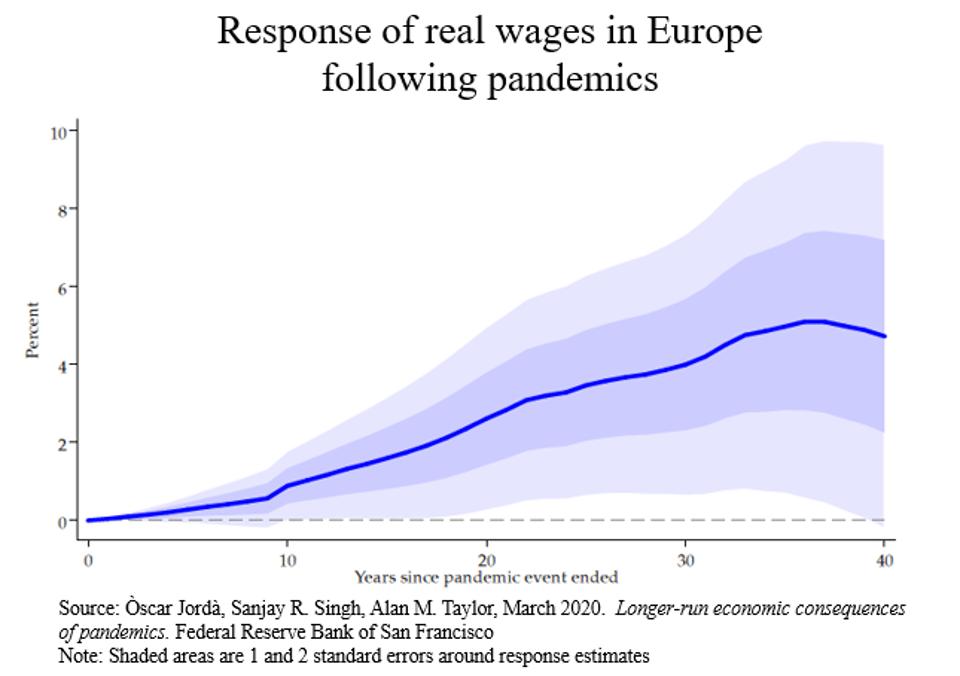

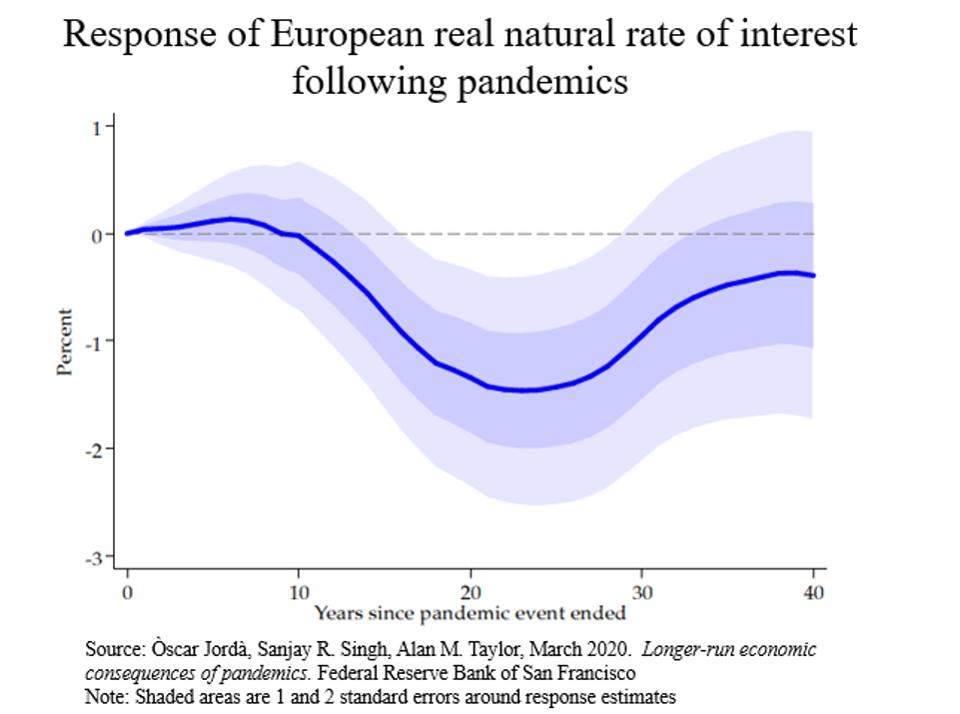

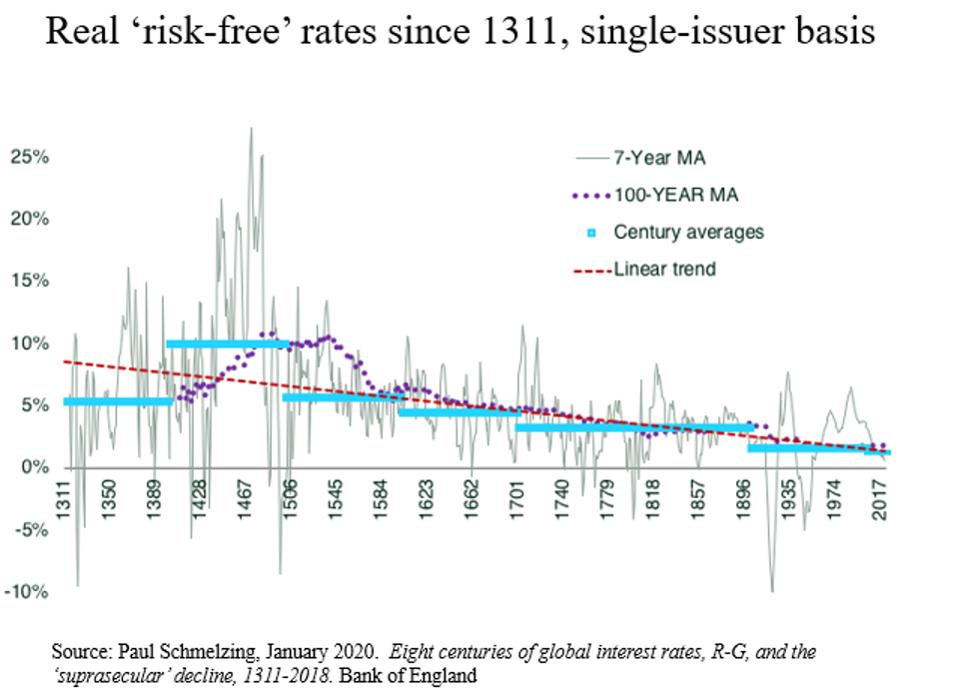

The conclusion from history is that pandemics give a boost to real wages but deliver disappointing real returns. Unlike other catastrophes, such as wars or natural disasters, demand for capital doesn’t experience a surge after pandemics, which in turn results in an extended period of modest real rates.

It is reasonable to assume that the aftermath of this current pandemic will also keep real rates contained. This is likely to encourage investing beyond the traditional asset mix with more of a tilt to alternative assets with equity-like returns.

This article first appeared in Forbes. This material contains opinions of the author, but not necessarily those of Sun Life or its subsidiaries and/or affiliates.